China Stock Market Outlook 2019

In our market forecast for 2018 [ You can read here], we instructed “Watch China! We have to get used to the idea that “When China sneezes, the world catches a cold.” – And this is what happened in 2018! China’s economy got in serious trouble and with some delay, the entire world seems to have been suffering or turned into panic mode, including the world largest economy, the United States!

In 2019, China and its economy are at a crossroads! More and more data suggests that China’s economy has been slowing down substantially. Whatever the reason might be, over-leveraging, bad management, or a prolonged trade-war with the US, China’s direction is clear – down!

Chinese stock markets have already led the way since early 2018, with Chinese stocks officially in a bear market territory as of January 2019. There is nothing to suggest that the course of the stock market has changed as of yet.

So what does that mean for emerging markets investors and investors betting big on China? Where will China’s economy be heading in 2019 and what will the Chinese stock market price in next? In this post, we look at the current state of China’s economy, stock market opportunities and the many risks that lie ahead for investors.

Time to Invest in China now? Don’t Get Your Hopes Up!

The short answer is: It will be bad for some time!

When Trump tweeted he had very good talks with Chinese president Xi Jinping in December 2018, the markets spiked. Trump told reporters before leaving the White House that the US is “close to doing something” with China to ease the ongoing trade war between the two countries.

Since then in an almost periodic fashion, we have heard more of these “close to doing something” type of tweets without any further details on how these good deals might actually look like.

Being an astute Trump skeptic on whatever he tweets, it always sounds more like a classic pump and dump scheme and trying to keep investors happy to prop up stock markets.

In other words, it has been expedient for Trump to make headline news of being close to making a “great” deal for the US, while the rest of the world has been shivering to pay the price (Japan, Taiwan). So, are the latest Trumps US-China deal announcement a fluke?

Yes, there is a positive newsflow as both parties assure the public their willingness to make a deal. But has anyone considered that the genie is out of the bottle a long time ago and it won’t get back in any time soon? How do you stop a moving oil tanker and on top of that reverse course by 180 degrees? Certainly not with one or two tweets or tooting your own horn!

China’s GDP Is Slowing Down

We all know the stories of phenomenal growth, cutting edge technology in key areas (e.g. A.I) and the advantages of centralized, top-down governments. But the fact of the matter is, China is going through a very natural, and for some experts long overdue, downward cycle, in a much longer growth trajectory.

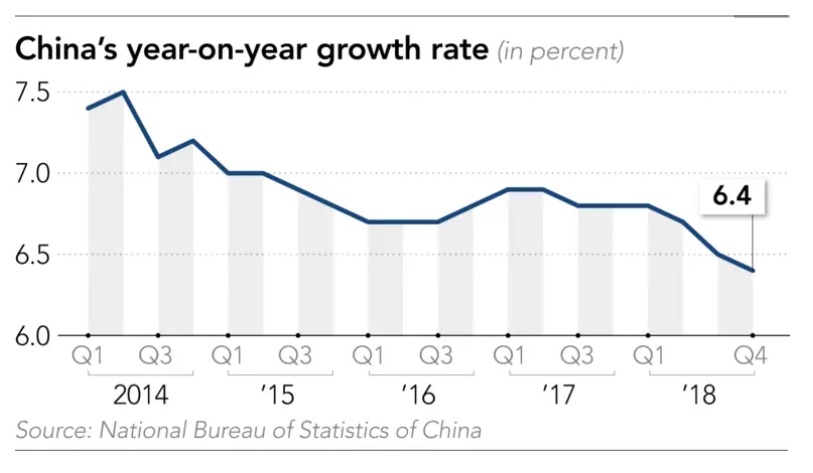

Just this Monday, China published the latest figures suggesting a continuous slow down of their economy. According to official data, the world’s second-largest economy grew 6.6 percent in 2018 — the slowest pace since 1990.

That number matched analysts’ expectations as the fourth quarter GDP growth was 6.4 percent, in line with the market consensus. But the question would be how reliable the data actually is that comes out of China without any further verification? How much have Chinese officials fudged the numbers to get to a pinpoint forecast?

We all know that the Chinese are well-versed in the art of window dressing and fine-tuning data for their own purposes and political agendas like anyone else in the world. Coming earnings season will bring light on these numbers as companies will have to report their last quarter results.

China’s Currency

China’s currency suffered its largest ever monthly fall against the US dollar in June 2018.

The renminbi weakened by 3.3% against the dollar in June 2018, the worst single-month decline since China established its foreign exchange market in 1994. According to state media, it was an “irrational overreaction” by speculators and investors alike.

China is not the only country that has been suffering from a declining currency against the USD. In our May issue, we mentioned the first signs in emerging market currencies, such as the Turkish lira, Brazilian real and Indonesian rupee.

What makes China’s currency decline so noteworthy is its decline against all other major currencies, indicating a general cooldown of China’s economy and reversal of capital flows out of China

The negative consequences of a declining Chinese currency could be devastating. Like any emerging market that finds itself in a financial death spiral, China would have to deal with accelerated capital flight, domestic liquidity tightening, and the possibility of increased credit stress. But China is not any emerging market – it’s the second-largest economy in the world.

For the time being, their immediate intervention to stabilize its currency seems to work, but for how long?

China’s Stock Markets

According to Chinese traders, corporate profits have worsened this year and are unlikely to improve against the backdrop of an economic slowdown. With the fluctuation of its local currency and the increased trade tensions with the US, Chinese stocks have also fluctuated widely – with a clear trend downward.

According to Chinese traders, corporate profits have worsened this year and are unlikely to improve against the backdrop of an economic slowdown. With the fluctuation of its local currency and the increased trade tensions with the US, Chinese stocks have also fluctuated widely – with a clear trend downward.

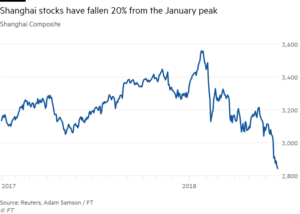

China’s Shanghai composite is tracking for its worst year in seven after falling 8% in June. A relentless six-week selling streak has sent the mainland’s benchmark stock index down 13.9%. From its peak in May, it has dropped over 20%, officially defined as a bear market territory.

Especially tech stocks have been suffering so far. Baidu, Alibaba and Tencent, also known as the BATs, have lost a combined $168 billion in value thanks to the US-China trade war, concerns over high valuations, and a regulatory crackdown from Beijing on social media and gaming companies. Alibaba shares are down over 20% last year, Tencent has plunged 22.4%, and Baidu is off more than 6%.

Investors in a dedicated China ETF such as the iShares MSCI China ETF (MCHI) administered by BlackRock might have seen a promising recover since the beginning of 2019 to $56, but over period of 1 year investors have lost substantially coming from a high of $77. Like so many post-shock recoveries, we worry that this could be one of the infamous sucker rallies with more losses in the making for overeager bargain hunters.

In summary, the escalation in trade tensions with the US, while deleveraging the financial system and cleaning up the shadow banking, might have been too much to chew on and the unwanted side effects have been growing larger that are now clearly visible.

The US-China Trade War – A Black Swan in Disguise

The wild card, of course, has been the prolonged trade dispute with the US. President Donald Trump’s tariffs on roughly $200 billion worth of Chinese goods kicked in, bringing the total amount of Chinese goods faced with tariffs up to approximately $250 billion, and it has threatened duties on double that value of products. In response, Beijing slapped tariffs on $110 billion in U.S. goods targeting politically important industries such as agriculture.

Since September 2018, it became apparent even to the most optimistic bull that the US-China trade dispute would not end any time soon and that it would have a definite impact on companies earnings, and general business sentiment. Especially companies that were lauded as immune suffered the most as their global outreach made them prone to global supply-chain bottlenecks – companies such as Apple or many semiconductor and car manufacturers among the victims.

The trade dispute had their wished for effect on China’s economy, at least from an US perspective. Chinese stocks were the first to blow the alarm in early 2018 and there hasn’t been a noteworthy recovery ever since suggestion more pain going forward.

As one official data after another confirms a slowdown of China’s economy the worst fears become a reality, something stock markets priced in months before, but the effects only now visible in companies earnings for the last quarter of 2018. But what is a possible way out of the rut? Is there some easy medicine for the patient?

After a December meeting between President Donald Trump and Chinese President Xi Jinping, the leaders of the world’s two largest economies agreed to a temporary truce while they sought an agreement within three months. The next round of negotiations is scheduled to take place at the end of January, when Vice-Premier Liu He travels to meet U.S. officials in Washington,

But the outcome at this moment is more than uncertain as both parties still seem to disagree on key points such as patent infringement or recognizing China as equal partner.

China’s Spending Dilemma

For years, party officials have been incentivized to force growth through production and export of cheap goods, regardless of the effects on prices, global macroeconomics or, for that matter, pollution. Only in October 2017, at the party conference had General Secretary Xi Jinping shifted emphasis.

China’s leadership talked of “three tough battles”: against preventing major risks (mainly financial – the new target is to be “further deleveraging”); poverty (Xi fancies a “moderately prosperous society” in all respects); and pollution (he wants to see the sky blue again).

China was curbing capacity to the global economy while focusing on stimulating domestic demand instead. According to close observers, the results have been instantaneous, as prices of natural gas (a “clean fuel”) doubled; steel output stalled, and the cement sector output actually fell even as demand for it (and hence prices) rose.

Financial reforms to deleverage and bring order into an opaque system of secondary lending markets (shadow banking) seem to have taken effect as well. Bankruptcies have increased dramatically. 2018 so far has been a record year of corporate bond defaults, already totaling more than three-fourths ($2.5 billion) of the previous high, according to official statistics.

We have already reported on Anbang’s very swift bankruptcy handling by Chinese authorities.

But now it seems everything is in reverse again – back to the old medicine!

We all know, that China has been eager to reverse course by doing the same of the old. According to the Nikkei Asian Review, “China is planning a record-high rail investment of around 850 billion yuan ($125 billion) this year, aiming to prop up a sputtering economy with stimulus measures that also include subsidies for car and appliance purchases.”

Also, Chinese banks that suffered under increased government scrutiny and tightening policies, have been regiven more liquidity options and green light to do much of the same as before – handing out cheap credit to anyone who asks for it. These are all policies that might have worked in the past, but will they work this time?

When you talk to any Chinese official in regards to stimulus packages and the lessoned learned from Japan’s bubble economy and policy blunders committed in the years that followed you might get the impression that they haven’t studied anything else. Yet, they seem to be doing the exact same mistakes or at least they will suffer a very similar fate.

The central government should listen to the warning that came from their own ranks. The former president of the Chinese central banks warned of a “Minsky Moment” the Chinese people could face if they continued on an irresponsible fiscal path without the necessary structural reforms.

China Outlook

From a psychological standpoint, all market players are nervous about the data coming out of China and the general mood is rather “risk off” than risk on again. Hopes for a quick recovery and a second spring for companies such as Tencent or other BAT companies is still high. But with each further market decline, that hope will shrink dramatically. Right now, China doesn’t really off an attractive risk-reward scenario for smart investors. The following key points should be considered if we are interested in investing in Chinese stocks:

1) It seems that the Central Government has little choice but to return to old policies if it doesn’t want to lose the initiative. But the world is a very different one than 10 years ago when China spent its way to the top of the world hierarchy.

Fact is, China has become a country with an extensive surplus to a debtor nation, thanks to giant building projects, fiscal stimulus packages, and expansion of their military capabilities. All the medicine worked well as the world was united to achieve growth and prosperity together – it won’t work in the coming years.

Reforms, painful adjustments, and restructuring projects are necessary this time to bring China’s economy to the final stage of its very impressive evolution to superstardom. The leaders at the top knew this, and they were prepared to make necessary adjustments. But then came along Trump…

The reason for their abrupt reversal of plans are the US-Trade disputes, China’s own black Swan so to say – but that shouldn’t be an excuse to continue the reform path especially for the shadow banking sector – otherwise, China’s leadership is risking all the fruits of their hard labor.

2) It seems both parties are eager to do a deal now, but just by assuring “willingness” to do a deal, does not constitute 1) an actual mutually beneficial deal 2) a return to old good times. On the contrary, any signs that global trade picks up again gives the FED the justification to continue their “normalization” policies. This alone will work as a cap to the promised land and a serious obsticle to speedy recovery for Chinese stocks or stocks in general.

We will know more in coming weeks as Trump’s and Xi Jinping’s negotiations teams are battling it out in a series of trade talks before the approaching deadline in March. However, for The Monthly Truffle, the outcome is clear already! Whatever trade deal will be struck, it’s already too late!

Even though many market experts, among them Fidelity Investments, see “very, very attractive” valuations among Chinese stocks, that doesn’t mean it can go much, much more attractive in the coming months. We recommend our Truffle subscribers to stay clear of China and Chinese stocks in 2019, as the massive Sucker Rally unfolds. There will be plenty of better opportunities to load up on Chinese stocks, securities ore direct investments down the road.

More Emerging Market News

For more emerging market news and specific investment recommendations subscribe to one of our premium investment newsletters!