How Vanguard Redefines Emerging Markets Investing

In the competitive world of retail and institutional money management, no other company has made a bigger impact than Vanguard. It’s one the of the largest asset managers in the world, it has the largest fund in the world as measured by assets under management (AuM), and it is the lowest cost provider of them all – all thanks to the revolution of index investing, (‘passive’ money management), and the visionary leadership of its now retired founder, John Bogle.

That Vanguard dominates money management for developed countries is widely known. With their wide range of index funds and ETFs, they long ago won the intellectual battle of passive vs. active money management. The result has been constant growth in assets under management, a wider range of product offerings, and a continuous increase of new clients worldwide.

But it doesn’t stop here. Vanguard is also making strong efforts to spread their influence beyond plain vanilla product offerings (such as S&P 500 index funds) into the broad field of frontier and emerging markets investing. Here, the battle of passive vs active fund management still rages, and Vanguard is on a quest to win the whole thing for itself.

In this installment of our emerging markets investing series, we look at Vanguard’s efforts to dominate emerging markets investing, and how investors could make use of their product line while profiting from all the advantages emerging markets offer to enterprising investors.

Emerging Markets Investment Management Companies

In a recent interview with Bloomberg, fund manager Robert Marshall Lee, of top-performing Newton Global Emerging Fund, commented on the passive vs active management debate:

“Competition from exchange-traded funds doesn’t even feature for me, I am very unconcerned…If you track the index you end up holding a lot of undesirable companies.”

The 22-year investment veteran based out of London has good reasons to be cocky. He had a good year in 2017, comfortably beating his emerging markets benchmarks by several percentage points.

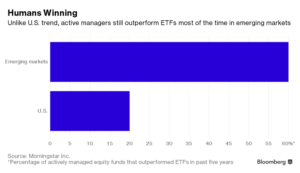

And he is not alone. Within emerging markets investing, that statistics indicate how for the last 5 years, stock pickers have beat passive emerging markets funds 60% of the time. The question is – for how long will this continue and how long does Mr. Marshall-Lee stay with his firm, where the average holding period of a senior fund manager in the City is three to four years or less?

And he is not alone. Within emerging markets investing, that statistics indicate how for the last 5 years, stock pickers have beat passive emerging markets funds 60% of the time. The question is – for how long will this continue and how long does Mr. Marshall-Lee stay with his firm, where the average holding period of a senior fund manager in the City is three to four years or less?

Emerging Markets Fund Management

Not to take anything away from Mr. Marshall-Lee, but there are good reasons to doubt his success going forward.

For one, emerging markets have become themselves more mainstream, and hence more efficient in processing investments and managing capital markets. This makes conventional stock picking more and more challenging.

On the other hand, the growing depth of low-cost passive managed index funds and ETFs from providers such as Vanguard will make life more difficult for traditional managers in emerging markets funds.

As index funds overran traditional money managers in developed countries, so will they overrun actively managed funds for emerging markets, as their sphere of influence increases and with that their entire range of operational advantages.

Star Fund Managers Come and Go

Someone who is certain of this is John Bogle, former head of Vanguard, and now celebrated guru of index fund investing. According to him, “It’s mathematically impossible to beat ETFs”. For him, it is only a matter of time before index funds and ETFs dominate emerging markets as well.

Besides, as with any institutionalized operation, emerging markets fund providers suffer from the same institutional imperatives as anyone else in the money management industry. The emerging markets investment industry is infamous for its very high management fees and the occasional blackouts by their star fund managers.

Whether Mark Mobius at Templeton or hybrid fund managers such as Anthony Bolton at Fidelity, the history of star fund managers for emerging markets is littered with dead bodies and broken dreams of former fund management celebrities.

Mr. Marshall-Lee has had a good run, but so did all the stars before him. The question is whether he will be able to avoid this one year that may ruin his stellar track records and ultimately his client’s confidence forever. The odds are strongly against him.

For now Vanguard and co. might be underperforming fast moving stock pickers from active fund management firms. But you can be sure that – Vanguard won’t be worried about any of this.

Vanguard Emerging Markets Funds

Besides offering the leading index funds for the most important benchmark indices of the world, Vanguard early on adopted emerging market indices, such as the MSCI and FTSE index funds for emerging markets. They were conveniently grouped as the Vanguard Emerging Markets Index group of products.

Besides offering the leading index funds for the most important benchmark indices of the world, Vanguard early on adopted emerging market indices, such as the MSCI and FTSE index funds for emerging markets. They were conveniently grouped as the Vanguard Emerging Markets Index group of products.

With some delay over its competitors such as BlackRock or StateStreet, Vanguard added a whole line of ETF products, including emerging markets ETFs. The blame for this delay lies with none other than John Bogle himself, an outspoken critic of ETFs.

He believes that ETFs induces unnecessary trading by both speculators and retail investors. Nevertheless, he wasn’t able to block the rising popularity of ETF trading. Vanguard’s new management saw no other choice but to jump on the speeding bandwagon of launching any conceivable ETF possible.

Here is an overview of Vanguard’s most popular equities emerging markets index funds and ETFs:

Vanguard Emerging Markets Stock Indexes (VEIEX/VEMAX)

This is Vanguard’s flagship emerging markets index fund, which is also available as Admiral Shares, and ETF. In its prospectus you can find the fund’s investment objective:

“The Fund seeks to track the performance of a benchmark index that measures the investment return of stocks issued by companies located in emerging market countries.”

The fees are moderate at 0.32% (expense ratio), and the minimum investment for retail clients is only $3,000.

At the time of writing, its fund size was over $100 billion, and its three largest holding was:

- Tencent Holdings Ltd.

- Taiwan Semiconductor Manufacturing Co. Ltd.

- Naspers Ltd

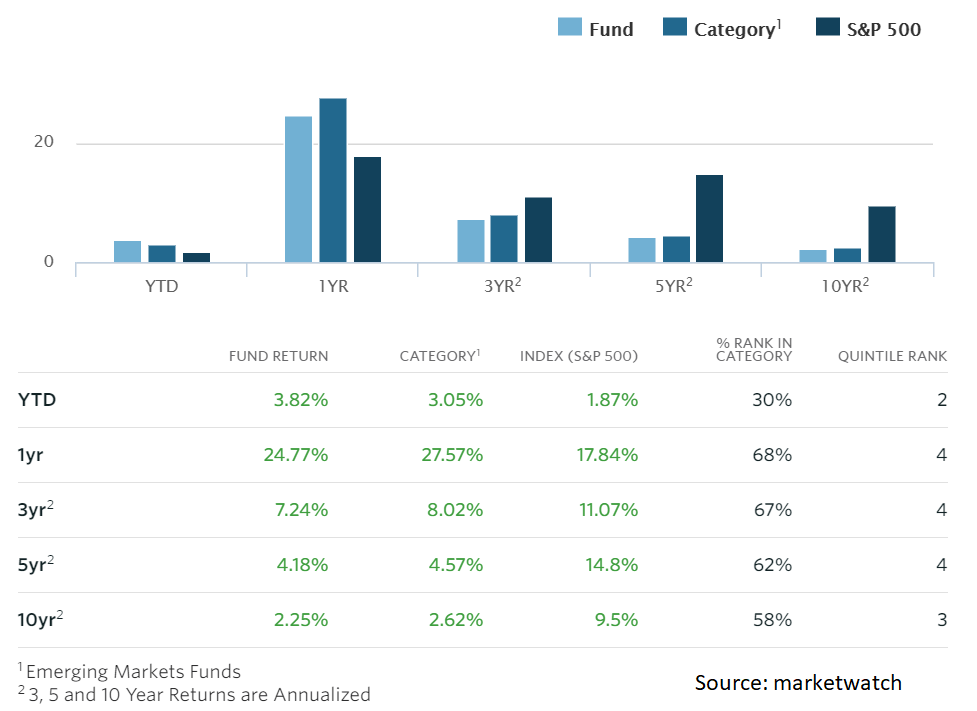

Alas, looking at its performance over the last 10 years, you will find a rather bleak picture. It wasn’t able to beat its peers in the active money management community, nor was it able to match the S&P 500’s 9.5% (2.25%) annualized performance – not even close. In short, you would have been much better off just buying the Vanguard S&P 500 index fund.

Vanguard FTSE Emerging Markets (VWO)

This Vanguard emerging markets ETF tracks the FTSE Emerging Markets Index. It is most likely the cheapest ETF for emerging markets retail investors can buy. With an expense ratio of only 0.14% it charges less than half the fee for its flagship emerging markets index funds the VEIEX, but with a very similar diversification and composition.

It holds over 4700 stocks and its three largest positions are identical to VEIEX:

- Tencent Holdings Ltd.

- Taiwan Semiconductor Manufacturing Co. Ltd.

- Naspers Ltd.

In its investment prospectus it states for its investment objective:

“The Fund seeks to track the performance of a benchmark index that measures the investment return of stocks issued by companies located in emerging market countries.”

More specific:

- Invests in stocks of companies located in emerging markets around the world, such as China, Brazil, Taiwan, and South Africa.

- Track the returns of the FTSE Emerging Markets All Cap China A Inclusion Index.

Unfortunately, it comes with an even more appalling performance track record than its close cousin the VEIEX. Over the last 10 years, it has only achieved 1.3% annualized returns.

Never Missing a Good Business Opportunity

Interestingly, Vanguard offers actively managed emerging funds as well. To hell with the whole childish debate over active vs. passive money management and futile ideologies when it comes to making a few more bucks.

Naturally, Vanguard’s actively managed funds come at a much higher management fee. For example, where their flagship emerging markets index funds charge 30 basis points, their actively managed equities funds for emerging markets charges 90 basis points.

For completion, we have added Vanguards flagship mutual fund for emerging markets actively managed by real professionals and stock pickers.

Vanguard Emerging Markets Select Stock Fund (VMMSX)

Asset class: International/Global Stock

Fund category: Diversified Emerging Markets

Management type: Active (Advised by Wellington Management LLP and other emerging markets specialists).

Minimum investment: $3,000

Expense Ratio: 0.90%

Fund total net assets: $819.5 million

Number of stocks: 314

Funds’ three largest holdings:

1 Taiwan Semiconductor Manufacturing Co. Ltd.

2 Tencent Holdings Ltd.

3 China Construction Bank Corp.

10 year annualized performance: 1.82%

Whether you choose a more traditional index fund or an ETF from the growing range of investment products that Vanguard offers depends on your own investment strategy, risk profile and how much involved you would like to get. Both options have specific benefits that can be incorporated into your personal asset allocation and long-term investment strategy.*

*Please consult with Vanguard or your private banker directly – without paying a high consultation fee.

Vanguards Competitive Advantage

For now, Vanguard Emerging Markets Funds may be underperforming its competition from the active management realm. But keep in mind – past performance is no indicator of future performance. Maybe Vanguard’s range of index funds and ETFs for emerging markets will see a roaring performance over the next 10 years, not only beating the S&P 500 but also its peers in the active money management community. It holds some aces up its sleeves and here is why:

For now, Vanguard Emerging Markets Funds may be underperforming its competition from the active management realm. But keep in mind – past performance is no indicator of future performance. Maybe Vanguard’s range of index funds and ETFs for emerging markets will see a roaring performance over the next 10 years, not only beating the S&P 500 but also its peers in the active money management community. It holds some aces up its sleeves and here is why:

A Firm without Stars

In a recent interview with Bloomberg News, Gerry O’Reilly gave a brief description and tour of Vanguard’s operations. O’Reilly is the senior portfolio manager at Vanguard, who oversees more than $800 billion in assets.

His main job is to make sure that Vanguard’s flagship fund, the Vanguard Total Stock Market Index Fund, matches the performance of its benchmark. What stands out is the efficiency of the 18 traders responsible for Vanguard’s entire U.S. portfolio – and their senior manager most clients have never even heard of.

This gives Vanguard an enormous competitive advantage over its peers in the active money management world. Everyone is replaceable without so much as a hiccup to Vanguard’s operations. Imagine Bridgewater Associates without Ray Dalio or Soros Funds without Soros. Expensive Star fund managers have no room in index fund operations.

In addition to not having to pay for armies of expensive star fund managers or research analysts, it has always had much lower marketing and advertising expenditures. It primarily operates on a continuous word of mouth campaign which has seen an increased momentum over the last three years throughout the world.

For Vanguard Big is Beautiful & Profitable

Today, Vanguard employs 15,000 people in 16 locations worldwide, managing about $5 trillion in assets. Cash is flooding into a growing range of index funds and ETFs that track indexes of every conceivable investment segment – including Vanguard’s own line of emerging markets products.

All this money helps keep operational costs low, and these savings are then passed on to clients in the form of reduced fees – the so-called ‘expense ratio’. With its growing asset size, Vanguard profited from economies of scale effect, which among others allowed it to negotiate fees paid to external third parties, such as brokers and banks.

Vanguard’s history of cost-cutting and reducing fees is impressive, and buying shares of Vanguard’s line of index funds is very affordable. In 2000, Vanguard was by far the lowest-cost provider, having slashed its expense ratio to 0.27 percent for its flagship funds, while the average fund charged 1.21 percent.

Through continuous investments in IT infrastructure and sophisticated software, Vanguard today is capable of charging only 3 to 4 basis points for some of its flagship funds to institutional clients and still operate very profitably. For retail clients, Vanguard charges $50 for a single share for its Vanguard Total Stock Market fund, with an initial minimum investment of $10,000.

Vanguard Emerging Markets – Destined for Success

It’s only a matter of time until index fund providers dominate emerging markets’ institutional money management as well. The days of traditional stock pickers at active fund management firms such as Robert Marshall-Lee or Mark Mobius (now retired) are counted.

The more emerging markets develop and grow, and the more emerging markets as an asset class is recognized in general, the more the advantage of passive money management will outshine those of active money management.

The fee differences today between passively managed and actively managed funds are so high (0.14 vs. 2.50 to 3.00%), that it is only a matter of time until the majority of investors interested in emerging markets investing will catch on.

Vanguard on a Mission

In Boston and New York, the large majority of professional money managers did not recognize the disruptive potential that the concept of index and ETF investing contained. It seems they do the same mistake for emerging markets investing.

In 2018, more and more traditional fund managers in the active only camp lose assets at an accelerating momentum. This includes firms such as Franklin Templeton or Fidelity while the leading providers of passive management absorb those assets their competitors are losing.

In this race for passive management dominance, Vanguard will play a very special role. It’s cost competitiveness, its growing brand awareness among institutional and retail investors, and its excellent global infrastructure are all excellent arguments in Vanguard’s favor.

Vanguard is, and remains, “the Walmart of money management,” In the mid to long-term, Vanguards structural and operating competitive advantages will break through in emerging markets investing as well.

Emerging Markets Investing – A Few Questions Remain

Some questions remain in our series of investing in emerging markets. For example, how to allocate to emerging markets, and how the 80/20 Investor sees the performance potential of emerging markets going forward. All these questions and more will be answered in our monthly premium newsletter: The Monthly Truffle.

On our blog will continue reporting on the development of specific emerging market countries and companies that offer great investment opportunities. Also, stay tuned when we have a closer look at Vanguard’s fiercest competitor: BlackRock.

Vanguard’s History

Vanguard originated out of a corporate power struggle at the top of Wellington Management, one of the oldest mutual fund companies in the USA, that took place between 1973 and 1975.

This power struggle, caused and lost by John Bogle, left this young and uprising star manager with only two options: Either leave Wellington or be demoted to take over the administrative functions, of Wellington Funds far away from the centers of power. Surprisingly, Bogle opted for the latter, but with some aces up his sleeve.

Wellington’s remaining board of directors didn’t think much of Bogle’s choice. In their eyes, he was out of the game and without any real power such as raising funds or managing money. However, they underestimated Bogle’s resolve and resourcefulness.

In May 1975, a new administrative entity was launched called Vanguard Group (The Vanguard Group of Investment Companies). It soon became apparent, that Bogle had much more in mind for this newly established entity than just doing mundane paperwork for his adversaries at Wellington.

Strangely enough, the Vanguards’ board, which was distinctly different from the board of the investment advisor Wellington, had more power to influence the day-to-day operations than anyone had anticipated. This new found power left Bogle with plenty of room to make life at Wellington more than complicated.

However, one problem remained for Bogle. Under contractual obligation, Bogle wasn’t allowed to actively raise money through traditional sales distribution channels or manage money.

So, how could he overtake vital management functions, while slowly detaching himself from Wellington? It dawned on him that the idea of creating the first index fund was the perfect solution to circumventing his agreements and a way out of his deadlock.

With passively managed index funds, he neither used an expensive sales and distribution network which was the traditional way of placing funds with clients. Nor would he actively manage any money – as technically no active advisory mandate was necessary for creating an index fund. After all, all he had to do was to copy a basket of stocks that represented an index such as the S&P 500.

The First Retail Index Fund

The plans took shape all through 1975 and finally, in August 1976 the Vanguard Group would launch the first publicly available index fund. The revolution was born and they would make their mark on money management history.

But initially, Bogle’s index fund met strong resistance from within and outside the money management community. Too strong were old believes and too hardened were the power ties of and an old-boys network that controlled institutional money management.

Including Wellington directors, many professionals ridiculed Bogle’s foray into passive investing, calling it “unpatriotic,” “Bogle’s Folly” or accusing the rationale behind passive management of aiming to be “average” – a very un-American ideology, indeed. By the end of 1976, the Vanguard fund had grown to only $14 million.

But entering the roaring 80s, Vanguard would collect more and more assets through more and more fund launches. Partially due to a recovering economy; partly because more and more investors understood the rationale behind passive management and its advantages over traditional and expensive money management operations.

By the beginning of the 1980s, Vanguard had collected $2.4 billion. By 1999, the year Bogle left as Chairman of Vanguard, the figure would swell to $540 billion. At the beginning of 2017, that number was about $4 trillion with new estimates of $5 trillion by the beginning of 2018.