What are the Risks for Index funds and ETFs

Not too long ago, I interviewed a hedge fund manager who uses a very quantitative approach to trading financial securities. I asked him his opinion about index funds and the answer he gave surprised me: “David, index funds are bets! Awful bets, with terrible odds. You could make 5[%], but eventually, you’ll lose 50[%].” I was ready to argue with him – until it struck me that managers and owners of hedge funds or any money pool are rarely on the losing side of the grand bet.

It’s their investors who take real risks, pay the fees, make bets, underperform and suffer the consequences. This got me wondering – how come? Are index funds really just plain money pools whose mission it is to copy the “natural” movements of an index? And you get rich just by default?

To understand the true nature of standard market index funds, we could approach this question from a different angle. Where do mutual funds or more specifically index funds fit in in the products and services universe?

Are index funds products or services?

Not really. A service is defined as “action of helping or doing work for someone.” If you go to a language school, take classes of any sort, or even get professional advice on matters of legal and medical nature, there are strict objectives, aims and outcomes. It either works or it doesn’t. You either receive something of real value, in the form of expertise solving a particular issue, or you don’t and you move on. One could argue that index funds make us rich and deliver on what they promise. But – first – they don’t promise anything, and second, they simply can’t deliver, or we all would be rich by now. They simply provide broad market exposure at low fees. It could be debated whether this is really a service that creates value for its clients if they experience 50% losses or more.

Are index funds providers of capital?

Again, not really. No mutual fund is a current medium of exchange in the form of coins and banknotes; nor are they a good store of value, as gold could be considered. You are not providing capital directly to any companies in an index. As Bogle himself noted in a recent interview with Bloomberg, “The stock market has nothing – n-o-t-h-i-n-g – to do with the allocation of capital. All it means is that if you’re buying General Motors stock, say; someone else is selling it to you. Capital isn’t allocated – the ownership just changes.”[i]

What can we infer from this? Index funds just don’t fall in any of those traditional categories that define our economy. So, if they are neither physical goods, money, or services, what are they?

As you might recall from other posts on Index Funds and ETFs, when you buy index funds you buy shares of a mutual fund. As mutual fund expert Birdthistle writes, “A mutual fund investment (…) is an equity arrangement. That is, fund investors are shareholders, not creditors nor account holders; they hold stock, not debt.”[ii] The consequences of this legal status are important because they permit substantial – even total – loss in the investment. If what you “own” goes down, you don’t have recourse to claiming anything back, because technically, you don’t own anything but a claim on an imaginary pot of money, and if that pot shrinks – tough. Here lies the fundamental danger of all index funds – they are not risk-free. As Bogle noted:

“[index] funds eliminate the risk of individual stocks, the risk of market sectors, and the risk of manager selection, with only stock market risk remaining (which is quite large enough, thank you).”

Index Funds and ETFs are Bets on Whole Equity Markets

What Bogle touched on is called “equity risk premium.” We should know by now, and from own experiences over the last 16 years that real markets just don’t follow the perfect models of economists. Since 2000, we have experienced two declines in US equities markets of more than 50%. If you concentrated in equity index funds and have no other allocation to bonds, real estate or cash, there wouldn’t be any other alternative than to deal with these declines. However, it doesn’t stop at equities. The same goes for any other major asset classes, including so-called “safe” bonds, commodities or real estate purchases. All of them can and will experience similar price declines in the future and from the looks of it, most likely at the same time.

So, what does this all mean? Well, the bottom line – and the single most important thing for you to remember about index funds – is this: When you purchase standard benchmark index funds, you purchase a “bet” – you’re betting that the index prices will rise. Granted, the bet might have a higher propensity to pay off the longer you hold it, but in the short-term, you will have to deal with the entire range of possibilities inherent in any price bet, including massive declines.

As we all know, the line between investing, speculating and gambling is a fine one, especially when we deal with Wall Street. In the end, prices are the main determining factor of your future profits. If you buy a US index fund, you make a bet on rising prices in the US, and furthermore, you make a bet on America – a bet on its business and industrial, political and financial system. Then again, there is nothing wrong with making bets, especially if it is on such patriotic causes as betting on your country. However, more naïve fund buyers convince themselves that they are grand investors in the businesses of corporate America. They are not! Neither are they providing capital nor are they really aware what goes on, on an operational level of 500 companies or more.

Index funds are the very epitome of playing Wall Street. You are making a price bet on the entire market that is controlled and powered by Wall Street. However, like in any bet, bets can go either way – they’re the ultimate psychological challenge. And so we come to my next point, which is that in addition to essentially being bets, index funds also have a very particular psychological impact, which further multiplies the number of people who buy in – and then cash out at the worst possible time.

Index Funds Risks

Imagine you are a passenger on an ocean liner in the cold and dark northern Atlantic – and the ship just hit an iceberg. As the vessel begins listing to one side, the captain tells everyone that the only way to survive is for all the passengers to move to one side of the ship and stay there. Anyone who leaves for the rescue boats might have a higher chance for survival individually, but as soon as the first person jumps overboard, it would seal the fate of the entire ship and everyone onboard. However, if they stay onboard, and the captain’s plan doesn’t work, they’re sure to drown.

What would you do if you were faced with such a dilemma? More importantly, what do you think everyone else would do? The index fund industry has long settled on their answer – stay on the damn ship. They tell you that you can be a winner, but only if you overcome your instincts and follow the advice of the mutual fund industry to stay for the long-term or, in Bogle’s own words, “Stay the course!” Unfortunately, hardly anyone seems to be listening. In the past, investors bought into stocks and funds as they were rising, and then, in market corrections, sold at very inopportune moments. They would take their money out and wait until the fund went up before buying again – the very opposite of the cardinal rule of investing: “Buy low, sell high.” As index fund proponent Charles Ellis, author of The Index Revolution, confirms: “The sad result is that investors time and again buy after a fund’s best results have been recorded and sell out after the worst performance is over.”[i]

It’s believed that our daily lives are largely determined by our insecurities and psychological misjudgments, especially when the topic of money is involved. Nobel Prize winner Professor Daniel Kahneman of Princeton University researched how decisions and mistakes are made. According to Kahneman, “If we think that we have reasons for what we believe, that is often a mistake. Our beliefs, wishes, and hopes are not always anchored in reasons.”[ii] In his studies, Professor Kahneman and his late colleague Amos Tversky realized that we have two systems of thinking. With their research, they opened a new branch of economics called behavioral economics. What they described was a world where our decisions and judgments are a result of a battle in our mind – a battle between deep-rooted instincts that manifest themselves through our intuitions.

Index Funds and Psychology

Seth Godin, the famous marketing guru, refers to this as the “lizard brain.” It controls our intuitive reactions and daily decision-making. It has evolved over millions of years into a very powerful control mechanism. According to Kahneman, “our thinking is riddled with systematic mistakes,” known among psychologists as cognitive biases. “They make us spend impulsively and be overly influenced by what other people think. They affect our beliefs, our opinions, and our decisions, and we are not even aware it is happening.”[iii] Add the investor’s itch (the impulse to be active because you might lose out), and you can see that we have a very interesting cocktail of powerful psychological forces that causes various forms of cognitive bias. When it comes to making decisions regarding money and putting it to work, it seems that our lizard brain too often takes hold of us, and with some very dire consequences.

One of the most interesting examples of psychology and investing converging is the aforementioned significance of price quotations, and the dramatic psychological feedback loops these can cause. They have been a never-ending source of psychological torment for generations of speculators, investors, CEOs, and economic policymakers. Prices impose themselves directly on our psyche. If you’ve ever found yourself checking your phone for price quotes several times a day, for something that should matter in 10 or 20 years, you’ll know what I’m talking about. Those already invested feel stimulated to invest more at higher prices, as they might be thinking of all the gains they are missing out on with their dormant cash at more or less 0% interest.

On top of all this, there is a familiar behavioral pattern when playing with “house money” – money from previous successful years – that isn’t part of the initial investment. In real gambling, the matter of general risk aversion quickly fades when punters gamble with house money. The same behavior pattern can be observed in financial markets, where people take more and more risks at higher prices as they feel they won’t lose their original investment – that the money they’re playing with is somehow “bonus cash.” As Richard Thaler writes in his book Misbehaving: “The house money effect – along with a tendency to extrapolate recent returns into the future – facilitates financial bubbles.”[iv]

Let’s look at recent trends. Since 2007, according to national surveys, the rate of households owning stock, through direct or mutual fund investments, has gone down from over roughly 65% to around 55% in 2015.[v] Not surprisingly, the rate improved somewhat from a low in 2013 of 52%, and it seems to be gaining momentum.

Always Behind The Curve – Nothing Has Changed

People who missed the rise in the stock market over the last five years were pressured to play catch up and jump on the indexing bandwagon. As a result, since March 2009, the S&P 500 increased more than 200%. According to Morningstar, in 2016, index funds experienced fund inflows of $625.2 billion, actively managed funds posted outflows of $92.3 billion, and the Dow Jones breached the 20,000 mark for the first time in its history.[vi] “One would do well to remember that this state of affairs is not a new phenomenon,” warns Steven Bregman, co-founder and president of Horizon Kinetics, an independent research firm specializing in inefficient markets. “In prior eras, it was known as go-go investing, or trend following. Now it takes the guise of index-based asset allocation.”[vii]

In fact, experience shows that most people didn’t invest in stocks until the rally was in its final innings. At the start of 1982, only $41 billion of the $241 billion in mutual funds was in equity funds; the remainder was in bond ($14 billion) and money market ($186 billion) funds. By the end of 1990, assets in bond ($291 billion) and money market ($498 billion) funds still outnumbered assets in stock ($239 billion) funds three to one.[viii] Only by the end of 1996 did assets in equity funds exceed that of their debt-oriented cousins. From this, it is fair to infer that many individual investors who dove into the stock market did so near the height of what was then a bubble, and probably enjoyed only a few years of solid returns before the 2000 crash. The same pattern had emerged before the subprime crisis brought the next rally to an end. After 2000, post the dot-com bubble disaster, equity ownership immediately dropped. Eventually, it reached a new high at over 65% at the peak of 2007, just before the housing market collapse.

It doesn’t help that the majority of investors have very idealistic return expectations of their index. Most pension funds in the US still expect 8% or thereabouts, according to a McKinsey Global Institute report published in 2016. The report states that customers expect “returns typically in the 7.5% and 8% range for a portfolio of stocks and bonds.” The conclusion of this report is that institutional investors and retail investors need to reduce their investment return expectations.

As Lewis Brahams, author of The House That Bogle Built, tactfully described it: “A similar pattern of the ignorant herd of investors stampeding into overvalued asset classes at the worst possible moment has recurred throughout history – from the eighteenth century’s Dutch tulip bulb craze until today’s housing bubble.” Part of the blame lies in the index funds and their providers, who have created a system of perpetual marketing that works almost too well in absorbing new money – and in compounding the potential impact of a potential collapse.

Index Funds & ETFs in 2019

There is nothing wrong with index funds or ETFs being simple bets on stock market directions. After all, we all should be participating in the growth of our economies to secure a safe and financially secure retirement. However, that all changes when there is no growth, or worse markets decline – and you know they do from time to time.

There is nothing wrong with index funds or ETFs being simple bets on stock market directions. After all, we all should be participating in the growth of our economies to secure a safe and financially secure retirement. However, that all changes when there is no growth, or worse markets decline – and you know they do from time to time.

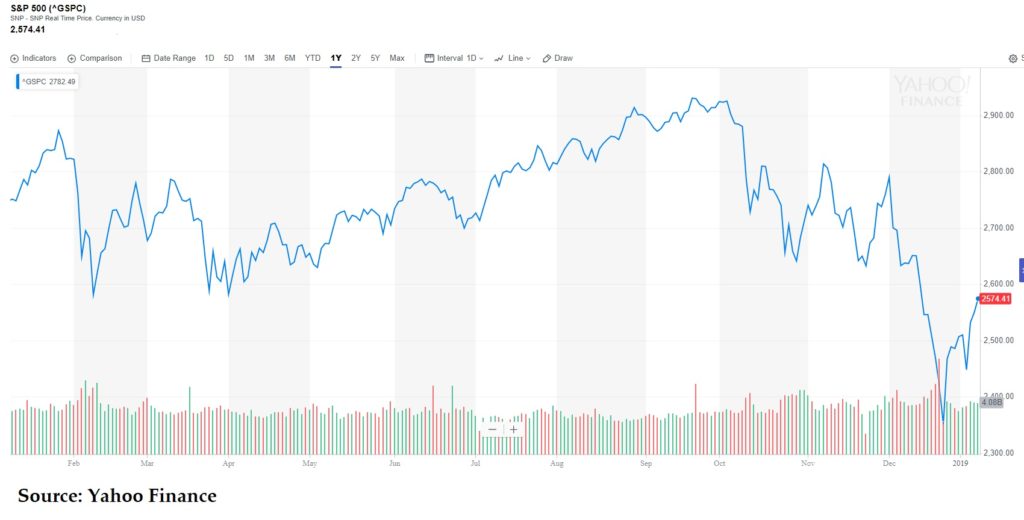

According to TrimTabs Investment Research investors are dumping stocks and corporate bonds at the end of 2018 at the fastest pace ever. So much for long-term investing and ignoring market ups and downs. Mutual funds which invested in equities and bonds lost a record $152 billion in December, while U.S. equity exchange-traded funds just had their first back-to-back weekly outflows since July 2018, shedding $7.1 billion in the last two weeks, according to the data service provider.

“Demand for US equity ETFs has been diminishing. The liquidity outlook for US equities remains downbeat. Our indicators remain neutral for the short term and outright bearish for the intermediate term,” David Santschi, TrimTabs’ director of liquidity research, said in a note Monday.

If this trend continues, guess who is getting really nervous? The US baby boomer generation, that has been preparing for retirement a while back would see itself in real trouble, should they experience similar market declines as 2008. In 2008 most benchmark index funds lost 50% from top to the bottom leaving those who were just retiring in real financial doldrums.

This time, it could be a whole different story (Read: Avoid the Sucker Rallies), but a story without a happy ending. Without the unprecedented money printing by central banks around the world, the holders of index funds and their ETFs might be waiting for a long time to see their bets recover to old highs.

This time we are just at the beginning of a great debt deleveraging and economic slowdown. Combine this with a new gospel of “our country first” and “distrust your neighbor”, we could see some very frothy stock market returns (if any) going forward.

You don’t have to be a predictive genius to understand where this leaves all those index funds and ETF believers. But then again, it could be completely different as bets can always go in both directions. In the end, Index Funds and ETFs are just simple financial tools to participate in stock market returns or losses, i.e. financial bets – nothing more and nothing less!

If you liked what you read here and want to know more about the fascinating world of Index Funds and ETFs, please consider purchasing the book on Amazon >>here<<

[i] Ellis, Charles D.. The Index Revolution: Why Investors Should Join It Now. (Hoboken: Wiley, 2016)

[ii] BBC. “How do we really make decisions?”. http://www.bbc.com/news/science-environment-26258662 (Accessed February 28, 2017)

[iii] Ibid.

[iv] Thaler.

[v] GALLUP. “Gallup’s annual Economy and Finance survey.” http://www.gallup.com/poll/182816/little-change-percentage-americans-invested-market.aspx (Accessed February 28, 2017)

[vi] Morningstar.com. “Indexing, Vanguard Drove Global Fund Flows.” http://sg.morningstar.com/ap/news/Market-Watch/156406/Indexing,-Vanguard-Drove-2016-Global-Fund-Flows.aspx. (Accessed February 28, 2017)

[vii] Yahoo Finance. “Analyst sounds the alarm on the ‘most crowded trade in investing history.” http://finance.yahoo.com/news/analyst-sounds-the-alarm-on-the-most-crowded-trade-in-investing-history-180954941.html. (Accessed February 28, 2017)

[viii] Braham, Lewis. The House that Bogle Built: How John Bogle and Vanguard Reinvented the Mutual Fund Industry. (New York: McGraw-Hill Education, 2011)